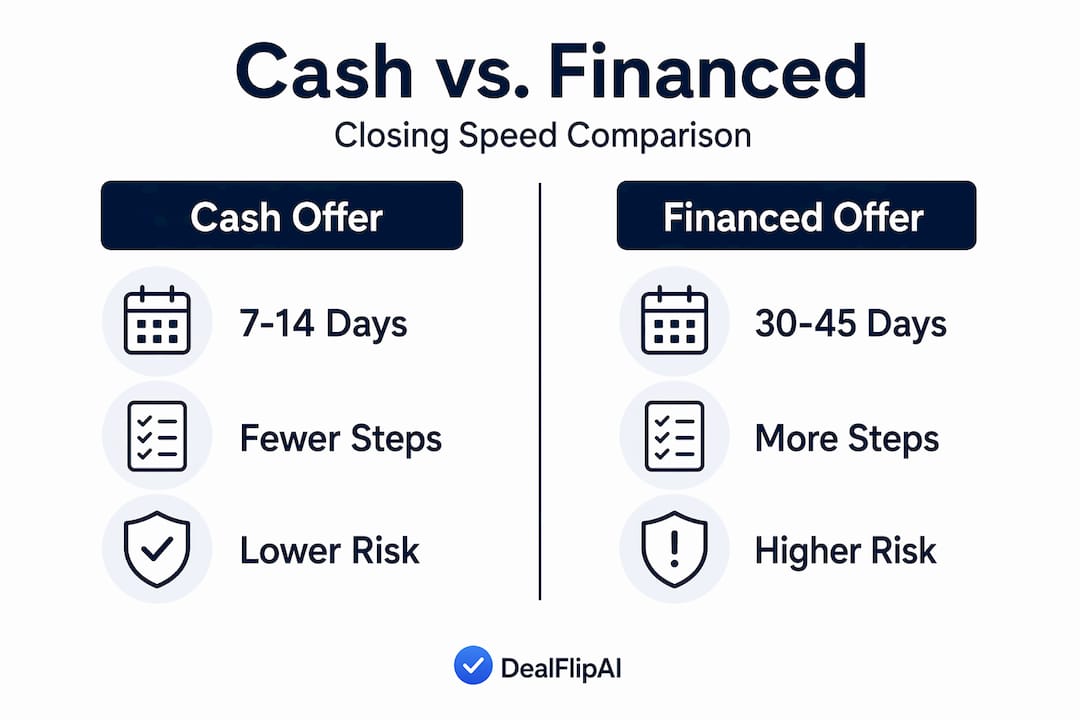

If you've ever wondered why cash offers close faster than traditional financed deals, you're not alone. Most sellers and investors assume the difference is minor, maybe a week or two at most. The reality is far more dramatic. Cash offers close in 7 to 14 days, while mortgage-backed transactions routinely take 30 to 45 days or longer. That gap isn't random. It's the direct result of eliminating an entire category of process steps that most buyers take for granted. This guide breaks down exactly why that happens and how you can use that knowledge to your advantage.

Table of Contents

- Key takeaways

- Why cash offers close faster than financed deals

- How cash buyers skip the bottlenecks

- Other factors that still affect cash closing speed

- Cash vs. financed offers: comparing timelines and trade-offs

- Practical tips for leveraging cash offer speed

- My take on cash offers after years of deal watching

- How Dealflip helps you evaluate cash offers faster

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Cash closes dramatically faster | Cash offers typically close in 7 to 14 days versus 30 to 45 days for financed offers. |

| Financing steps are the main bottleneck | Underwriting, appraisal, and income verification add weeks to financed closings that cash buyers skip entirely. |

| Proof of funds replaces lender approval | A proof of funds letter confirms buyer ability, giving sellers confidence without waiting for a bank. |

| Title and escrow still take time | Even cash deals require title clearance and escrow coordination, so plan for those steps. |

| Price and speed involve trade-offs | Cash offers often come in lower, so sellers must weigh speed and certainty against maximum sale price. |

Why cash offers close faster than financed deals

The single biggest reason why cash offers close faster comes down to one word: underwriting. When a buyer uses a mortgage, the lender doesn't simply hand over money because the buyer says they can afford it. The bank runs its own independent review of the buyer's finances, the property's value, and the overall risk of the loan. Mortgage underwriting adds 30 to 45 days after an offer is accepted, and that's under normal circumstances without any complications.

The mortgage approval process breaks down into several distinct stages, each with its own timeline:

- Application and processing: The buyer submits financial documents, tax returns, pay stubs, and bank statements. The lender's processing team reviews these for completeness.

- Appraisal: The lender orders an independent appraisal to confirm the property is worth the loan amount. Appraisers are often backlogged, adding days or even weeks.

- Underwriting: An underwriter reviews everything and decides whether the loan meets the bank's standards. They can request more documentation at any point, resetting the clock.

- Conditional approval and final sign-off: Even after initial approval, underwriters often issue conditions that require additional paperwork before giving final clearance.

Each of these steps depends on third parties. Appraisers, title companies, and underwriters all have their own schedules. If any one piece of information is missing or inconsistent, the whole process stalls. A buyer whose employer gives a slightly different job title on a verification letter than what appears on their application can trigger a week-long documentation request.

Pro Tip: If you're selling and considering a financed offer, ask your agent for the buyer's pre-approval letter and check whether it's a full pre-approval or just a pre-qualification. Pre-qualification carries far less certainty and can signal a longer, riskier closing.

How cash buyers skip the bottlenecks

Cash closings speed up transactions not by moving paperwork faster, but by eliminating entire loan approval bottlenecks altogether. When there's no lender involved, you remove multiple stages from the process in one stroke. Here's what that looks like in practice:

- No lender approval required. The buyer doesn't need a bank's permission to close. There's no underwriting timeline to wait on, no conditions to satisfy for a third party.

- No appraisal contingency. Lenders require appraisals to protect their investment. Cash buyers don't have that requirement, so the property's appraised value becomes a negotiation point rather than a deal barrier.

- No income or employment verification. Lenders verify that buyers can sustain mortgage payments over decades. Cash buyers prove their ability differently.

- Proof of funds replaces lender verification. A proof of funds letter shows the seller that the buyer's money actually exists and is accessible. It's a bank statement or equivalent document, reviewed in minutes, not weeks.

- Fewer contingencies overall. Cash offers typically eliminate financing and appraisal contingencies, removing the most common reasons deals fall apart after acceptance.

The result is a closing process that can realistically happen in 7 to 14 days when everything lines up. Some cash transactions close in as few as seven days when title work is clean and both parties are prepared. Compare that to the 30 to 45-plus day standard for financed offers, and you start to see why sellers and investors place such a premium on cash.

Pro Tip: As a seller, request proof of funds within 24 to 48 hours of accepting a cash offer. Speed in early verification sets the tone for the entire closing and catches any issues before they become expensive delays.

Other factors that still affect cash closing speed

Here's something most sellers don't hear enough: cash doesn't mean instant. While cash removes financing risk, non-financing risks like title or property issues remain and can slow closings just as much as a lender problem.

The steps that remain in every cash closing include:

- Title search and clearance: A title company must verify there are no liens, unpaid taxes, or ownership disputes attached to the property. If a contractor filed a lien two years ago that the seller forgot about, that has to be resolved before closing.

- Escrow coordination: Even without a lender, an escrow company typically holds funds and coordinates the transfer of documents between parties.

- Inspection (if included): Cash buyers often waive inspection contingencies, but many still request one. The results can trigger renegotiation.

- Deed preparation and recording: The legal paperwork transferring ownership must be prepared, signed, notarized, and recorded with the county.

The table below shows what stays and what goes in a cash closing compared to a financed one:

| Step | Financed offer | Cash offer |

|---|---|---|

| Mortgage application | Required | Not applicable |

| Underwriting | Required (2 to 6 weeks) | Not applicable |

| Bank appraisal | Required | Optional/negotiable |

| Proof of funds | Not required | Required |

| Title search | Required | Required |

| Escrow coordination | Required | Required |

| Inspection | Usually required | Negotiable |

Skirting lender contingencies means sellers face fewer last-minute deal derailments and gain real confidence in their closing date. But you should still budget time for title and escrow. A realistic cash closing timeline is 10 to 14 days when you account for these remaining steps.

Cash vs. financed offers: comparing timelines and trade-offs

Understanding the advantages of cash transactions means looking at the full picture, not just speed. Here's a direct comparison of what each type of offer means for sellers and investors.

| Factor | Cash offer | Financed offer |

|---|---|---|

| Typical closing time | 7 to 14 days | 30 to 45 days or more |

| Deal fall-through risk | Low | Moderate to high |

| Appraisal required | No (typically) | Yes |

| Financing contingency | None | Present |

| Typical offer price | Often 5 to 10% below market | At or above market |

| Seller carrying costs | Lower (shorter timeline) | Higher (longer holding period) |

| Certainty of close | Very high | Moderate |

The price trade-off is real and worth taking seriously. Cash buyers often offer less to account for the risk they absorb and the speed advantage they provide. A buyer paying all cash takes on the full risk of property value movement during the transaction and has no lender safety net. That risk gets priced into their offer.

For sellers, the math depends on your situation. If you're carrying two mortgages, relocating for a job, or dealing with an estate sale, the speed and certainty of a cash offer can easily be worth accepting a lower price. If you're in no rush and the market is competitive, holding out for a financed offer at a higher price may make more sense.

The negotiation in cash deals often shifts focus from financing approval to terms balancing price and speed. Sellers who understand this dynamic can negotiate more effectively, asking for a faster closing in exchange for a slight price concession, or holding firm on price when the buyer's timeline isn't urgent.

Practical tips for leveraging cash offer speed

Knowing why cash deals close quickly is useful. Knowing how to act on that knowledge is where the real advantage lives. Here's how to put it to work as a seller or investor.

- Verify proof of funds immediately. Don't accept a cash offer without requesting a bank statement or proof of funds letter within the first day. Speed here shapes the entire closing because delays in verification push everything else back.

- Order your title search early. As a seller, you can order a preliminary title report before you even list. This surfaces any liens or ownership issues before a buyer finds them, keeping your closing on schedule.

- Work with experienced parties. Experienced cash buyers and agents close faster and with fewer complications. First-time cash buyers may still include contingencies or misunderstand the process.

- Set a clear closing date in the contract. Cash closings are flexible, but "as soon as possible" is not a timeline. Nail down a specific date in the purchase agreement and work backward to coordinate title and escrow.

- Use technology to vet offers. AI-based tools that analyze offer credibility, deal risk, and buyer signals can help you assess whether a cash offer is legitimate and likely to close on time. Tools that cross-reference deal scoring and valuation give you a faster read on offer quality.

Pro Tip: If you receive competing cash and financed offers, ask your agent to calculate the net proceeds from each after accounting for holding costs during the longer financed closing. A cash offer that looks lower on paper may actually yield more money in your pocket.

My take on cash offers after years of deal watching

I've seen sellers get so excited about a cash offer that they skip asking the obvious questions. Who is this buyer? Where does the money actually come from? Is the proof of funds current?

The phrase "cash offer" carries a kind of psychological weight in real estate that sometimes short-circuits rational thinking. Sellers hear it and assume speed, certainty, and simplicity all in one package. That's often true. But I've watched cash deals drag on for three to four weeks because a buyer couldn't produce clean proof of funds, or because a title search turned up a lien that took two weeks to resolve.

The real insight I've gained from watching dozens of these deals unfold is this: faster closing with cash comes from removing lender processes, not from eliminating legal due diligence. The sellers who close the fastest with cash buyers are the ones who prepare their end of the transaction before they even receive an offer. Their title is clean, their documentation is ready, and they have a good agent or tool helping them evaluate offer credibility on day one.

Technology is genuinely changing how fast cash closings happen. Sellers who use AI-assisted offer evaluation tools get a much clearer read on which cash offers will actually close and which ones will waste their time. That kind of preparation used to require expensive professionals. Now it's available to anyone who knows where to look.

My honest advice: don't treat a cash offer as a guaranteed win. Treat it as a strong starting point that requires the same due diligence you'd give any offer, just with a faster clock.

— Apex

How Dealflip helps you evaluate cash offers faster

If you're analyzing deals as a reseller or real estate investor, the same principles that apply to cash home offers apply to every transaction you evaluate. Speed matters. Certainty matters. Knowing whether a deal is worth pursuing before you waste time on it matters most of all.

Dealflip is built for people who need to make fast, informed decisions about whether a deal is worth taking. The AI offer suggestion tool helps you calculate the right opening number based on real market data, so you're not guessing when speed is on the line. The platform's deal scoring surfaces risk and profit potential together, giving you the full picture in seconds. Combine that with the free reseller tools to plan your logistics and calculate fees, and you have everything you need to move confidently on the best opportunities before anyone else does.

FAQ

How quickly can a cash offer close?

Cash offers typically close in 7 to 14 days, though some transactions close in as few as seven days when title work is clean and both parties are well-prepared.

Do cash offers always beat financed offers?

Not always. Cash offers are faster and carry less risk of falling through, but they often come in at a lower price. Sellers need to weigh speed and certainty against maximum sale price based on their specific situation.

What is a proof of funds letter?

A proof of funds letter is a document, usually a bank statement, that confirms a cash buyer has enough money available to complete the purchase. It replaces lender approval in a cash transaction.

Can cash closings still be delayed?

Yes. Even all-cash deals require title clearance and escrow coordination, and both can cause delays. Title issues like liens or ownership disputes are the most common reasons cash closings take longer than expected.

Why do cash buyers offer less than market value?

Cash buyers price in the risk and speed advantage they provide. By closing quickly and removing financing contingencies, they take on more risk than a buyer backed by a lender, and they reflect that in their offer price.