Fair market value (FMV) is defined as the price at which an asset would change hands between a willing buyer and a willing seller, both fully informed and under no pressure to complete the deal. This standard applies across taxes, real estate, insurance, estate planning, and legal disputes. Understanding what fair market value is used for helps you price assets correctly, avoid IRS penalties, and make confident buying or selling decisions. Whether you are selling a home, donating property, or flipping items on Facebook Marketplace, FMV is the benchmark that keeps transactions fair and defensible.

What is fair market value used for in asset pricing?

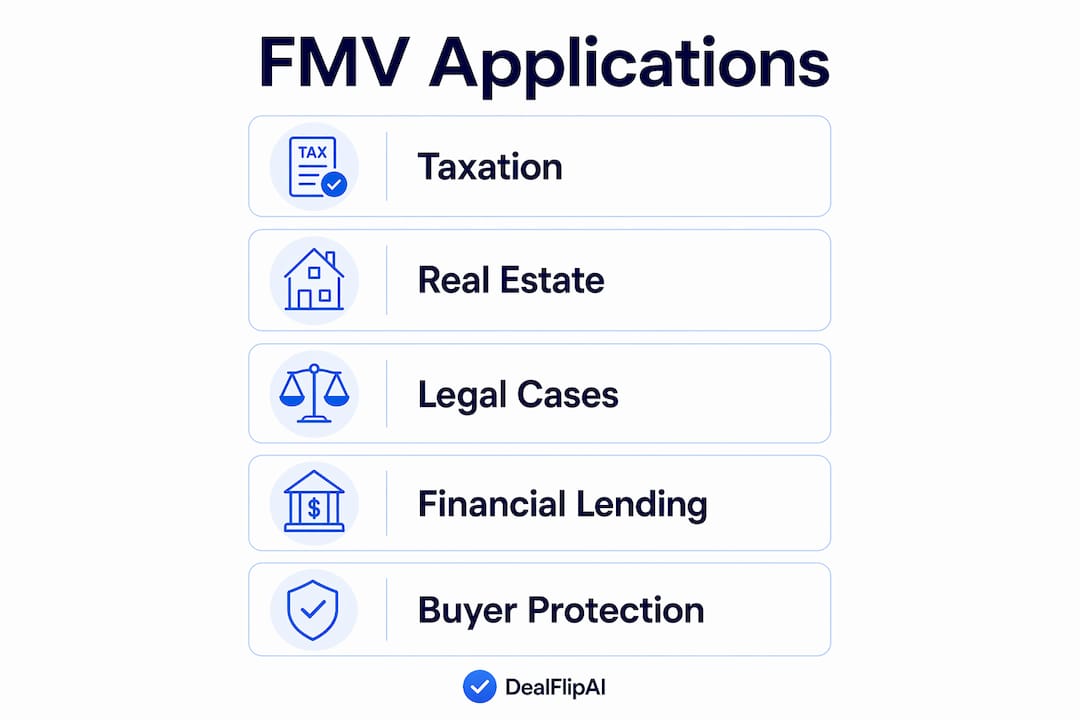

FMV is the foundational pricing standard used by the IRS, courts, appraisers, and financial institutions to establish objective asset worth. FMV serves as a benchmark for taxes, estate planning, real estate, insurance, and legal matters. That reach makes it one of the most widely applied concepts in personal finance and property transactions.

The IRS relies on FMV to calculate capital gains taxes, gift taxes, and estate taxes. Real estate agents use it to set listing prices. Insurance companies use it to determine replacement coverage. Courts apply it in divorce settlements and bankruptcy proceedings. In every case, the goal is the same: an objective, market-supported number that neither party can reasonably dispute.

FMV also protects you as a buyer. When you know an asset's fair market value, you can spot overpriced listings immediately. That knowledge is especially useful on platforms like Facebook Marketplace, where prices vary widely and sellers often list above actual market rates.

How is fair market value determined?

Appraisers use three standardized methods to calculate FMV, and IRS Revenue Ruling 59-60 remains the foundational framework guiding which approach applies to each asset type. No single method works for every situation. Professional appraisers typically apply at least two methods and reconcile the results into one defensible figure.

The three main approaches are:

-

Market approach (sales comparison): The appraiser identifies recent sales of comparable assets and adjusts for differences. This method applies to residential real estate, vehicles, and publicly traded securities. It is the most intuitive method because it reflects what actual buyers paid in the open market.

-

Income approach: The appraiser estimates the present value of future income the asset will generate. This method dominates for rental properties, businesses, and any income-producing asset. A rental property generating $24,000 per year, for example, is valued by capitalizing that income stream at a market-appropriate rate.

-

Cost approach: The appraiser estimates what it would cost to replace the asset from scratch, then subtracts depreciation. This method suits unique properties, specialized equipment, and assets with no active resale market.

FMV is not a fixed number but a range reconciled by expert appraisers explaining the most relevant method per asset. The reconciliation step is where professional judgment matters most. An appraiser weighs each method's reliability for the specific asset and arrives at a single, supported conclusion.

Pro Tip: Distressed sale prices, such as foreclosure auctions or urgent divorce-driven sales, are excluded from FMV calculations. The IRS and courts reject these as non-arm's-length transactions because compulsion distorts the price.

How does fair market value differ from related concepts?

FMV is frequently confused with book value, liquidation value, fair value, and investment value. Each term means something different, and mixing them up leads to costly mistakes.

-

Book value vs. FMV: Book value is an asset's historical purchase cost minus accumulated depreciation recorded on a balance sheet. FMV estimates current market price, not historical cost. A machine purchased for $50,000 ten years ago may have a book value of $10,000 but an FMV of $35,000 if the market for that equipment has held strong.

-

Liquidation value vs. FMV: Liquidation value is what you get when assets are sold quickly under pressure, often at a steep discount. FMV assumes no urgency and a reasonable exposure period. Liquidation value is always lower than FMV for this reason.

-

Fair value vs. FMV: GAAP guiding principles require fair valuation in financial reporting, which is sometimes called mark-to-market accounting. Fair value under accounting standards can differ from FMV under IRS standards because the two frameworks serve different purposes.

-

Investment value vs. FMV: Investment value reflects what a specific buyer would pay based on unique synergies or strategic goals. FMV excludes premiums for strategic value or investment synergies, focusing on a general market participant's perspective. A competitor acquiring your business might pay a premium above FMV because the deal creates synergies for them specifically.

The concept of the hypothetical buyer is central to all of this. FMV strips away personal circumstances and asks: what would a typical, informed market participant pay? That hypothetical framing is what makes FMV a neutral, legally defensible standard.

| Concept | Basis | Compared to FMV |

|---|---|---|

| Book value | Historical cost minus depreciation | Usually lower than FMV |

| Liquidation value | Forced or urgent sale price | Always lower than FMV |

| Fair value (GAAP) | Current market price for reporting | Similar but different legal standard |

| Investment value | Buyer-specific synergies and strategy | Often higher than FMV |

Practical uses of fair market value for buyers and sellers

FMV shows up in more financial decisions than most buyers and sellers realize. Getting it right protects your money. Getting it wrong can trigger audits, legal disputes, or bad deals.

-

Tax compliance: The IRS requires FMV for calculating capital gains when you sell property, gift taxes when you transfer assets, and estate taxes when assets pass to heirs. Informal estimates often face rejection by tax authorities, which means a formal appraisal is not optional for high-value transactions.

-

Real estate transactions: Buyers use FMV to avoid overpaying. Sellers use it to price competitively without leaving money on the table. Lenders use it to set mortgage amounts. A comparable market analysis is the standard tool for estimating FMV in residential real estate.

-

Insurance coverage: Property insurance policies are typically written to cover FMV or replacement cost. Knowing the difference matters when you file a claim. FMV-based policies pay what the market would give you for the asset, not what it costs to buy a new one.

-

Charitable donations: The IRS requires a qualified appraisal for donated property valued above $5,000. The deduction is based on FMV, not what you originally paid.

-

Legal disputes: Courts apply FMV in divorce asset division, bankruptcy proceedings, and business partner buyouts. A formally documented FMV protects you if the other party challenges the number.

Correct FMV also prevents the most common and expensive mistake buyers make: paying a price that reflects the seller's emotional attachment rather than actual market conditions. When you anchor to FMV, you negotiate from facts, not feelings.

Common pitfalls when applying fair market value

The biggest mistake buyers and sellers make is treating the last transaction price as FMV. Taxpayers often mistake last transaction price for FMV, and the IRS requires FMV to be consistently supported by evidence and formal appraisal. A single sale, especially a distressed one, does not establish market value.

Watch out for these common errors:

- Relying on informal estimates: Rules of thumb, online price guides, and neighbor opinions are not FMV. They are starting points at best. Relying on them for tax filings or legal matters creates serious risk.

- Ignoring market conditions: FMV changes as markets move. An appraisal from two years ago may not reflect current conditions, especially in volatile real estate or used goods markets.

- Confusing asking price with FMV: A seller's listing price reflects what they want, not what the market will pay. These two numbers are often far apart.

- Skipping USPAP compliance: The IRS expects documented, USPAP-compliant valuation reports for tax and estate purposes. USPAP stands for Uniform Standards of Professional Appraisal Practice, the national standard for appraisers in the United States.

Pro Tip: For any asset valued above $5,000 that affects your taxes, hire a certified appraiser who produces a USPAP-compliant report. The cost of a professional appraisal is almost always less than the cost of an IRS audit or a legal challenge.

Distressed transactions like foreclosures or divorce-driven sales yield prices below FMV and must be adjusted or discarded for FMV calculations. Courts and the IRS reject these as non-arm's-length sales because the seller was under compulsion. Always verify that comparable sales you use were arm's-length, open-market transactions.

Key Takeaways

Fair market value is the price a willing, informed buyer and seller agree on without pressure, and it serves as the legally required standard for taxes, real estate, insurance, and legal disputes.

| Point | Details |

|---|---|

| FMV definition | The price between a willing buyer and seller, both informed, under no compulsion. |

| Three valuation methods | Market, income, and cost approaches are reconciled to produce one defensible FMV figure. |

| FMV vs. related concepts | Book value, liquidation value, and investment value all differ from FMV in important ways. |

| Key practical uses | FMV governs tax filings, real estate pricing, insurance, charitable donations, and legal disputes. |

| Avoid informal estimates | USPAP-compliant appraisals are required by the IRS for high-value tax and estate matters. |

Why FMV matters more than most buyers realize

Walsh Pex, editorial contributor

After years of watching buyers and sellers navigate pricing decisions, the pattern I see most often is this: people treat FMV as a formality rather than a tool. They get a number, file their paperwork, and move on. That approach works until it doesn't.

The most useful shift I've seen is when buyers start treating FMV as a hypothesis to test, not a fact to accept. You get an appraisal, then you cross-check it against the market approach, the income approach, and recent comparable sales. If the three methods converge, you have a solid number. If they diverge significantly, that gap tells you something important about the asset or the market conditions.

I've also seen sellers consistently overvalue assets because they anchor to what they paid, not what the market will bear. Book value and emotional value are real to the seller. They are invisible to the buyer. FMV cuts through that disconnect.

My practical recommendation: for any transaction above $10,000, get at least two independent data points before agreeing on a price. For anything that touches your taxes, get a formal appraisal. The cost is small. The protection is significant.

One more thing worth saying directly: FMV is a hypothetical benchmark, not a contract price. The actual sale price can be above or below FMV depending on negotiation, timing, and buyer motivation. Knowing FMV gives you a reference point. What you do with that reference point is where skill and preparation come in.

— Walsh Pex

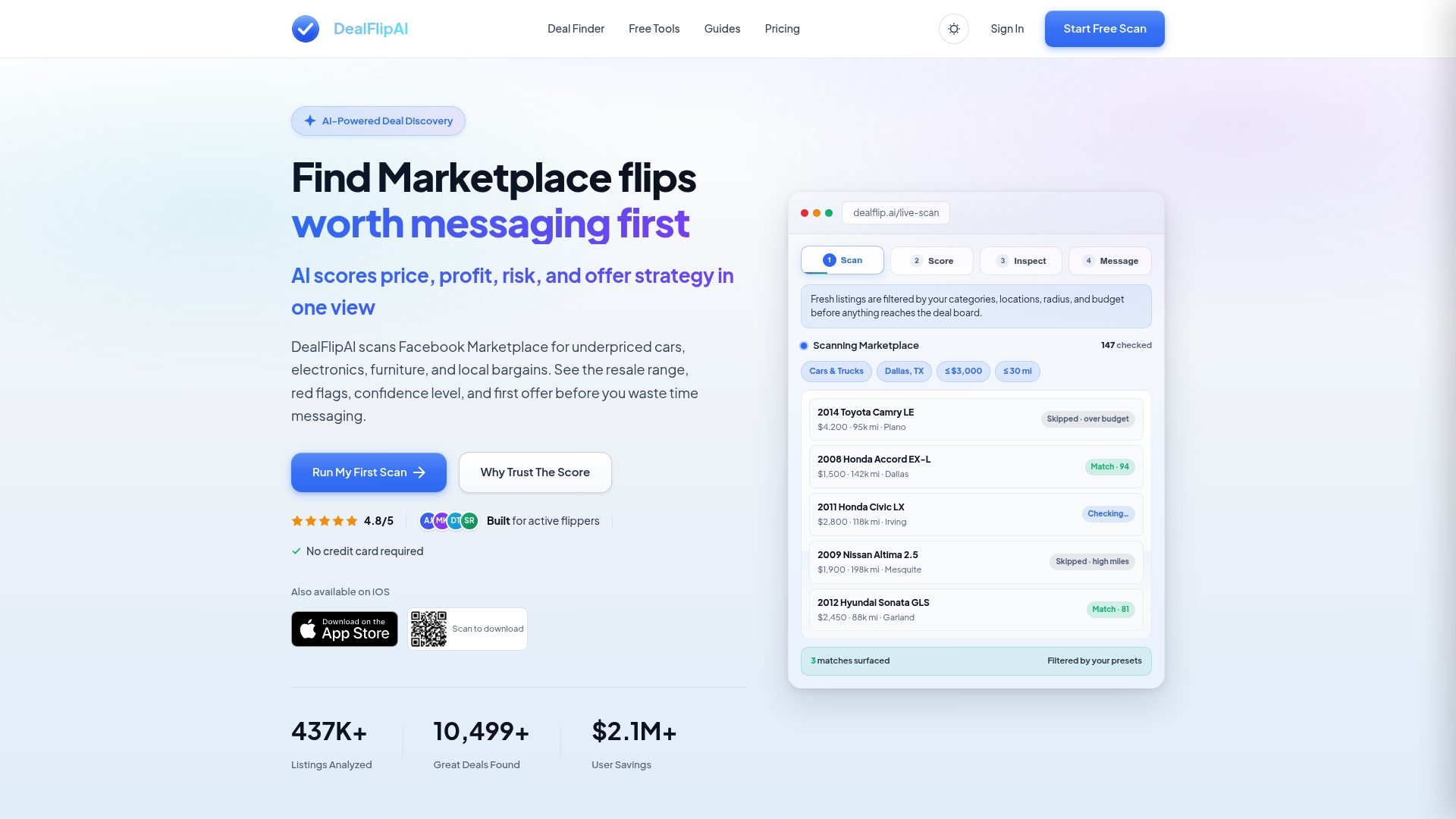

Dealflip AI helps you estimate fair value on marketplace deals

Knowing FMV theory is one thing. Applying it to a real listing in real time is another challenge entirely.

Dealflip AI is built for buyers and sellers who want data-backed pricing decisions on Facebook Marketplace. The platform scores listings by price, profit potential, and risk factors using AI, so you can see at a glance whether a listing is priced at, above, or below market value. The Facebook Marketplace Value Estimator gives you a fast, market-informed estimate for any item you are evaluating. If you want to find undervalued listings before other buyers do, the Facebook Marketplace Deal Finder surfaces deals that match your criteria in real time. Dealflip AI turns FMV knowledge into a practical advantage every time you shop or sell.

FAQ

What is the fair market value definition?

Fair market value is the price at which an asset would sell between a willing buyer and a willing seller, both fully informed and under no compulsion to transact. It is the standard used by the IRS, courts, and appraisers across the United States.

How is fair market value determined for real estate?

Real estate FMV is most commonly determined using the market approach, which compares recent sales of similar properties in the same area. Appraisers adjust for differences in size, condition, and location to arrive at a supported value.

Why are distressed sales excluded from FMV?

Distressed sales, such as foreclosures or urgent divorce-driven sales, reflect compulsion rather than open-market conditions. The IRS and courts reject these transactions as non-arm's-length sales that do not represent true FMV.

What is the difference between FMV and book value?

Book value is an asset's historical purchase cost minus accumulated depreciation. FMV reflects current market price, which can be significantly higher or lower than book value depending on market conditions.

When do you need a formal FMV appraisal?

A formal, USPAP-compliant appraisal is required by the IRS for charitable donations of property above $5,000 and for estate and gift tax filings. Informal estimates are routinely rejected in tax and legal proceedings.